The Quiet Engine: Why Your Wealth Grows While the News Screams

In the world of BigLaw, your day is too often defined by "The Noise." It’s the urgent email at 11:00 PM, the shifting regulatory landscape, and the constant hum of immediate crises that require your specific brand of high-octane problem-solving. It’s easy to start believing that everything important, including your wealth, must be just as loud and fast-moving.

But if you look at the data, the reality of wealth creation is much quieter. It doesn’t happen in the daily "shocks" of the financial news cycle; it happens through a persistent, structural force that operates behind the scenes while you’re busy billing hours.

I recently reviewed a compelling paper by Duncan Ashworth, The Invisible Hand of Corporate Efficiency, which provides a data-based look at why broad US equity markets have historically outperformed inflation. It’s a perspective that most financial news (read: financial entertainment) outlets ignore because it isn't dramatic enough for a headline. I’ve invited Duncan to share his research below, and then I’ll break down what this means for your personal financial strategy in 2026.

The Invisible Hand of Corporate Efficiency

By Duncan Ashworth (Guest Contributor) with light edits for compliance by Matt Smith (Founder and Lead Advisor of Concert Financial Planning, LLC)

Introduction

Over the last fifteen years, equity markets in the United States have delivered returns that far exceed what would be expected from inflation alone. While these outcomes are often attributed to innovation, globalization, or accommodative monetary policy, such explanations do not fully account for the magnitude, persistence, and statistical regularity observed in long-term market trends.¹ This paper argues that a deeper and more durable force—corporate efficiency—has been the dominant driver of equity appreciation. By examining long-term data from broad market proxies, this analysis shows that systematic gains in productivity and resource utilization have compounded into valuation growth well beyond inflationary effects.²

Data Sources and Methodology

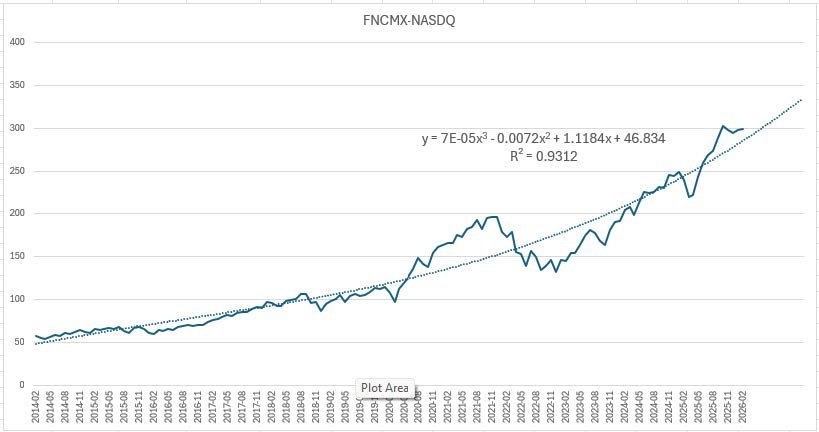

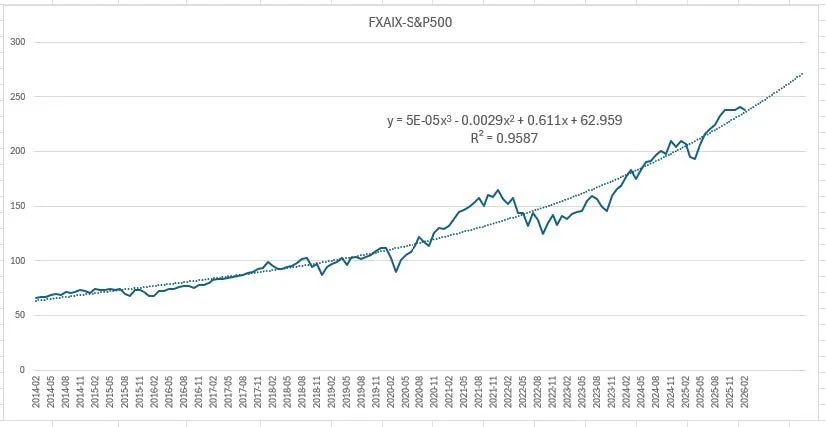

This analysis uses approximately fifteen years of monthly price data from two Fidelity mutual funds: FNCMX as a proxy for the NASDAQ Composite Index, and FXAIX as a proxy for the S&P 500 Index. Third-order polynomial trend lines were applied using Microsoft Excel to capture non-linear growth and acceleration. The resulting fits were strong: FNCMX produced an R² of 0.9312, while FXAIX produced an R² of 0.9587, indicating that long-term market behavior is highly structured rather than random.

Figure 1. FNCMX (NASDAQ Proxy) with Third-Order Polynomial Trend Line (R² = 0.9312)

Figure 2. FXAIX (S&P 500 Proxy) with Third-Order Polynomial Trend Line (R² = 0.9587)

Inflation as a Baseline

Over the same period, cumulative inflation would have increased nominal prices by approximately 38.5%³. Under this assumption alone, FNCMX would be valued near $78.81 and FXAIX near $91.56.

Under an "inflation-only" assumption, the cumulative price increase for these two mutual funds over this period would have been approximately 38.5%. However, observed market values exceed these levels by a wide margin, demonstrating that inflation alone cannot fully explain the growth trajectory.

Corporate Efficiency as the Primary Driver

Corporate efficiency refers to producing equal output with fewer resources, or greater output with the same resources. Advances in automation, software, logistics optimization, global supply chains, and data analytics have driven sustained productivity gains.⁴ These gains are structural and cumulative. Once achieved, efficiency improvements are rarely reversed, allowing productivity benefits to compound across business cycles.

Sources of Deviation from the Ideal Trend Curve

While the polynomial trend lines capture long-term behavior, real markets deviate from the ideal curve for several reasons: Monetary tightening or easing cycles; exogenous shocks such as pandemics or geopolitical conflicts; behavioral factors including fear, exuberance, and herd behavior; and sector-specific regulatory or technological disruptions.⁵ These forces introduce volatility around the trend but do not alter the underlying efficiency-driven trajectory.

Counterarguments and Rebuttal

A common counterargument attributes market growth primarily to accommodative monetary policy or valuation expansion. While low interest rates can elevate asset prices, they do not explain the sustained increase in earnings per unit of capital.⁶ Valuation multiples fluctuate, but efficiency improvements permanently increase cash-flow-generating capacity. The persistence and statistical strength of the trend lines suggest a real productivity phenomenon rather than a purely financial one.

Forward-Looking Opinion

If corporate efficiency continues to improve—particularly through artificial intelligence, robotics, and automation—my opinion is that the long-term trend suggests continued real growth above inflation.⁷ While short-term volatility is inevitable, the structural trajectory implies that equity markets will increasingly reflect productivity rather than labor or material intensity.

Conclusion

The divergence between inflation-only expectations and observed equity values over the last fifteen years points decisively to corporate efficiency as the primary explanatory force. This invisible hand operates quietly but relentlessly, shaping markets through compounding productivity gains.

Footnotes

By Duncan Ashworth (Guest Contributor)

¹ Gordon, R. J. (2016). The Rise and Fall of American Growth. Princeton University Press.

² Solow, R. M. (1957). Technical Change and the Aggregate Production Function. Review of Economics and Statistics.

³ U.S. Bureau of Labor Statistics, CPI-U historical tables.

⁴ Brynjolfsson, E., & McAfee, A. (2014). The Second Machine Age. W. W. Norton & Company.

⁵ Shiller, R. J. (2015). Irrational Exuberance. Princeton University Press.

⁶ Bernanke, B. (2015). The Courage to Act. W. W. Norton & Company.

⁷ OECD (2023). Artificial Intelligence, Productivity, and Growth.

APPENDIX

By Duncan Ashworth (Guest Contributor)

Why Financial News Skews Negative Even When Markets Rise

It often feels like financial news is overwhelmingly negative—even during long periods when major market indices such as the S&P 500 trend steadily upward. This perception is not accidental. Several structural, psychological, and economic forces bias financial media toward pessimism.

Human psychology is wired for bad news People are far more sensitive to losses than gains, a phenomenon known as “loss aversion”. A market decline captures attention more powerfully than a comparable rise. Negative stories trigger fear and urgency, emotions that hold attention longer. Media outlets, competing for attention, naturally lean into this bias.

Gradual market growth is not news Markets typically rise slowly and predictably over time. This steady compounding is expected and lacks drama. News organizations instead focus on deviations from the trend—crashes, shocks, and disruptions—which feel urgent and headline-worthy.

Mismatch of time horizons Markets create wealth over years and decades, while news operates on minutes and days. The drivers of long-term growth—earnings expansion, productivity gains, innovation, and reinvestment—are diffuse and slow-moving, making them difficult to package into daily headlines. Negative events, by contrast, are immediate and discrete.

Fear converts better than reassurance From a business standpoint, warnings generate more engagement than reassurance. Headlines emphasizing risk, danger, or uncertainty attract more clicks than those suggesting stability. Even balanced articles often feature pessimistic headlines.

Financial journalism emphasizes risk over return Risk is actionable and time-sensitive; return is statistical and long-term. As a result, coverage focuses on inflation, recession, geopolitical conflict, and valuation concerns, while the steady process of wealth creation remains largely invisible.

Markets fall sharply but rise quietly Most trading days are modestly positive or flat. A small number of sharp declines dominate investor memory and media coverage. This asymmetry causes rare downturns to overshadow frequent gains.

Cultural caution favors pessimism Optimism in finance can feel irresponsible, while pessimism appears prudent. Being wrong on the upside is more socially acceptable than missing a major risk. This cultural bias reinforces negative framing.

Conclusion: A perception gap Financial news functions more like a radar system than a progress report. Its purpose is to identify storms, not celebrate clear skies. While markets tend to move up over time, media coverage remains focused on threats to that trend. Understanding this distinction helps investors maintain perspective amid constant warnings.

Back to Matt

Why BigLaw High-Performers Fall for the Noise

Duncan’s research confirms what many of us suspect: the "noise" of the news is almost entirely disconnected from the structural growth of your portfolio. But as a high-performing attorney, you have a unique vulnerability. Your career is built on identifying and mitigating risks immediately. When you see a headline about a market "crash," your professional instinct is to do something.

However, in the world of long-term wealth, "doing something" in response to the noise is often the most expensive mistake you can make.

Here is the reality for your wealth in 2026:

Your Efficiency is Your Asset: Just as corporations grow by optimizing resources, your wealth grows when you optimize your time. Spending your Saturday morning trying to "time" a market entry or exit is a low-marginal-return activity for someone with your billable rate.

Structural Gains Require Patience: Corporate efficiency gains (like those from AI and automation) take years to compound into valuation growth. If you react to the "daily storm" identified by the news radar, you risk missing the "clear skies" of the underlying trend.

The Professional Advantage: The most successful attorneys I know have realized that they are not macroeconomists. They focus on their "Highest Marginal Return" - their practice and their family - while delegating the "financial plumbing" to a fiduciary who understands the difference between a temporary shock and a structural shift.

The "Invisible Hand" is doing its job. Your job is to stay out of its way and ensure your financial plan is built to capture that quiet, relentless growth while you focus on the work only you can do.

Ready to take control of your financial future?

Concert Financial Planning is a flat-fee financial planning firm built exclusively for BigLaw attorneys. If you're ready to talk through your situation with a CFA®/CFP® Professional who understands your career, compensation, and lifestyle, then schedule a free discovery call.